End the Paycheck-to-Paycheck Struggle: Actionable Strategies for 2025

If you've ever reached the end of the month with less than $100 in your account and no clue where your money went, you're not alone. In fact, a 2023 survey by LendingClub found that 60% of Americans still live paycheck to paycheck. I used to belong to that group. In 2022, I was earning $45,000/year and still ended most months with overdraft fees.

But by following a few key steps, I managed to not only break the cycle but build a $12,000 emergency fund within two years. This guide is built from real experience and backed by trusted financial advice from experts like Dave Ramsey and the CFPB. This will help you learn how to stop living paycheck to paycheck.

Let’s dive in and help you reclaim control of your money, one step at a time.

1. What You’ll Need to Stop Living Paycheck to Paycheck

Before diving into the steps, here’s what you’ll need to set yourself up for success. Consider this section the part where you gather all the ingredients before cooking. It’s hard to make progress without the right tools and mindset.

- A complete list of your income and monthly expenses

- Access to a spreadsheet (like Google Sheets) or budgeting apps like YNAB or EveryDollar

- An emergency-only savings account.

- 30 minutes weekly for money check-ins

- Discipline in managing every cent

- Openness to changing spending habits and boosting income

2. How to Stop Living Paycheck to Paycheck: Your Simple Action Guide

If you're wondering how to stop living paycheck to paycheck, these practical steps will help you take control of your money, build savings, and reduce financial stress starting from today.

Step 1: Get Clear on Your Finances

The first step to breaking the cycle of living paycheck to paycheck is gaining a clear understanding of your financial situation. That means reviewing every part of your money flow:

- Income: Include all sources, your salary, side gigs, freelance work, and any passive income.

- Fixed Expenses: These are regular monthly bills like rent or mortgage, utilities, insurance, and subscriptions.

- Debts: Note down all your debt payments, such as credit cards, student loans, or personal loans.

- Variable Spending: This includes everyday expenses that change month to month, like groceries, transportation, and entertainment.

To make this easier, use tools like Google Sheets or personal finance apps like Mint to map out your cash flow visually. For a beginner-friendly option, check out the free budget template from the Consumer Financial Protection Bureau (CFPB).

Personal tip: When I first started tracking my finances, I was shocked to find I was spending over $250 a month on food delivery. I had assumed it was just part of my grocery budget, but it was eating into my savings without me realizing it. Gaining clarity helped me make better choices moving forward.

Step 2: Create a Simple Budget

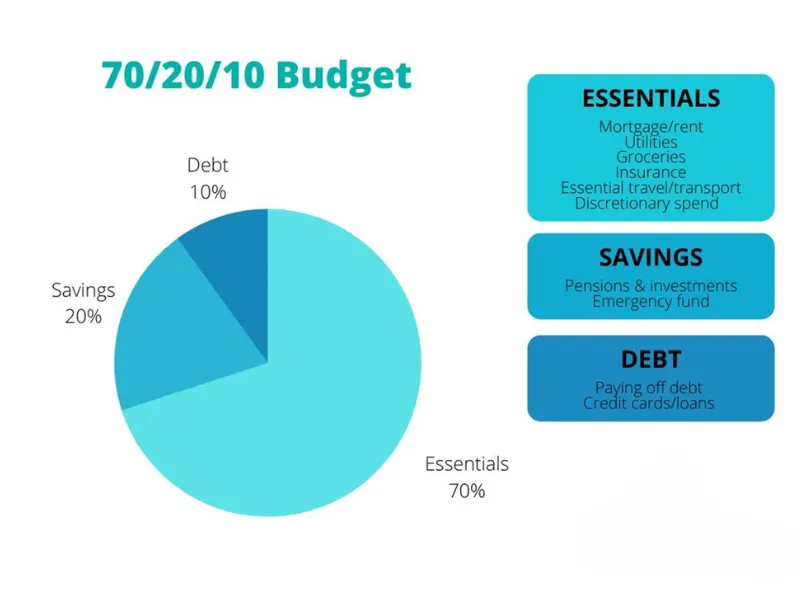

To take control of your finances, start by picking a budgeting method that works well with your lifestyle and financial situation. One simple and effective approach is the 70/20/10 rule:

- 70% for essential needs: This includes rent or mortgage, groceries, transportation, and other necessary living expenses.

- 20% for savings or paying off debt: This portion goes toward building an emergency fund, saving for the future, or reducing what you owe.

- 10% for personal wants: Use this for entertainment, dining out, hobbies, or anything non-essential that brings you joy.

Example: If your monthly income is $3,000, this breakdown would give you $2,100 for needs, $600 for savings or debt payments, and $300 for wants.

However, your situation might be different. Flexibility is essential. For instance, I personally started with an 80/15/5 split because my rent was unusually high. It's okay to adjust the percentages to match your current expenses. Revisit your budget monthly and make changes as your circumstances evolve.

Step 3: Track Every Expense

Another key to mastering how to stop living paycheck to paycheck is building awareness. That begins by tracking your spending every day or every week.

You can choose any method that fits your style:

- Use budgeting apps such as PocketGuard or Spendee

- Keep a pen and notebook handy to jot down expenses

- Or update a spreadsheet regularly

Why this works: Tracking helps you notice unnecessary spending. These are often small expenses between five and fifteen dollars that you may not think twice about, but add up quickly over time. This could include extra snacks, coffee runs, or subscriptions you forgot about.

Real example: Once I started tracking my spending, I discovered I was paying for three services I no longer used. Canceling them saved me forty dollars each month, which I now set aside for savings.

Step 4: Cut Non-Essential Spending

One simple but powerful strategy is to apply the 72-hour rule. When you want to buy something that is not urgent, wait three days before making the purchase. In most cases, the urge will pass, and you will realize you did not really need it.

Here are a few easy changes that can help reduce spending right away:

- Cancel memberships or subscriptions you no longer use

- Cook meals at home more often (batch cooking can help save both time and money)

Result: After making just a few of these changes, I cut back on dining out and saved one hundred eighty dollars in my first month. Small adjustments like these can make a big difference.

Step 5: Prioritize Essentials ("The Four Walls")

According to personal finance expert Dave Ramsey, known for his “Baby Steps” method, your top priority should be paying for the basics that keep you safe and stable. These include:

- Housing

- Utilities

- Transportation

- Food

Always take care of these expenses before anything else. Doing so protects your ability to live, work, and stay healthy.

Expert insight: The Consumer Financial Protection Bureau also recommends putting essential needs and secured debts first. This helps you avoid serious consequences like eviction, utility shutoffs, or losing access to transportation.

Step 6: Build a Mini Emergency Fund ($500–$1,000)

Begin by setting a clear goal to save between five hundred and one thousand dollars for unexpected expenses. This small financial cushion can help you avoid using credit cards or borrowing when surprise costs appear.

Start with simple actions:

- Sell things you no longer need

- Cut one regular expense and put that money into savings

My experience: I sold my bicycle and saved three hundred dollars. After that, I set aside fifty dollars each month until I reached one thousand.

Keep your emergency savings in a separate bank account. This makes it easier to resist the temptation to spend it on non-essentials. Save it for real emergencies only.

View more: https://h2tfunding.com/how-to-stop-living-paycheck-to-paycheck/

Nhận xét

Đăng nhận xét